- Buy-Side Insights Newsletter

- Posts

- Buy-Side Insights No. 12

Buy-Side Insights No. 12

● TUSK CFO Episode Drop — My First "Buffett Punchcard" ● My Professional Investment Journey ● Job Board ● What is Alpha? ● Top 10 Learnings from Steve Cohen's Interview

Doug Garber

July 14, 2025

Now Available:

● $TUSK ( ▼ 0.64% ) CFO Interview Episode Drop: Cigar butt morphing into a compounder. 50% of NAV and pivoting to higher return industries. And my first “Buffett Punchcard.”

● My Professional Investment Journey

● Job Board: New launch seeking: L/S Industrials, L/S Materials, and L/S Quantamental

● What is Alpha? What is left over after the factors. An overused word for residual or unexplainable quant stock movement.

● Top 10 Learnings from the GOAT HF Trader — Steve Cohen’s Goldman Sachs interview. Must love the game.

On Deck:

🔜 “Fumblerooski” at $VSTS ( ▼ 2.73% ) ? Dividend cut, guidance pulled right before the new CEO starts and right before his stock prices.

🔜 Jonathan Kasen: From Fidelity PM to Hilliards Chocolate entrepreneur — inspired by a dicey car ride with chauffeur Warren Buffett!

🔜 Exclusive interview with Doug O’Laughlin, President of SemiAnalysis — the premier semi industry consultants.

EP 007: TUSK – Cigar Butt Morphing into a Compounder: 50% of NAV & Pivoting to Higher Return Industries

In the latest episode of Pitch the PM, Doug welcomes Mark Layton, CFO of Mammoth Energy Services (NASDAQ: TUSK), to explore one of his highest conviction investment ideas and his first of twenty lifetime “Buffett punchcard” investments. This small cap company ($132 MM market cap) is valued below cash levels ($150 MM) with the market giving the company no credit for its existing businesses or underutilized equipment that was recently valued at $145 MM by an independent appraiser.

The company recently exited its largest industrial business for $110 MM (more than 3x MOIC), has its land drilling rigs held for sale and subsequent to the recording of this episode sold its frac assets for $15 MM. Mammoth, with the help of its largest shareholder — Wexford, is targeting 25-35% unlevered IRR’s in the aviation rental space where it has a robust pipeline. The company is also incubating its engineering, fiber, and rental equipment businesses.

Doug views this as a private equity investment in a public shell without the fees.

Pitch The PM's Variant View Investment Checklist:

What is my HISTORY with the stock, company and bias?

- Accumulated stock earlier in the year.

- Previously, invested in 2024 ahead of the 2024 PREPA settlement and sold after the company used the proceeds to reinvest in frac equipment.

1. What ACTION do I want the Portfolio Manager to take?

- I own shares and it is my first “Buffett Punchcard”

(Note: Small cap with low liquidity stocks may not be suitable for you)

2. Do I UNDERSTAND this business?

- Covered company since IPO

- OFS & Industrial investment specialist

3. Is the stock available at a REASONABLE price today?

- Yes, at $2.66/share or 95% of current unrestricted cash levels of $2.81, pro forma for the T&D sale

- At a 35% discount to line of sight cash (+$1.02 to $3.83) including the energy equipment divestments and the expected LOC/escrow releases.

- Then there is another $2.45/share of equipment value that was recently appraised

- less $0.28/share for the Puerto Rico tax liability net of the PREPA A/R owed

=$6.00/share NAV

- However, earnings are nil as most of the company’s value is in cash and public company costs absorb the profit from the businesses being incubated

4. Why is this stock MIS-PRICED?

- Historically, the company’s earnings and returns were driven by the volatile oilfield service (OFS) industry where capital was destroyed, particularly in frac and frac sand

- The company has started to pivot out of OFS into higher return industries

- The company is trading at 95% of current pro forma unrestricted cash levels as the market does not understand the new strategy in my opinion

5. What is the VARIANT VIEW vs the street?

- TUSK is no longer predominately an energy company in my view

- The company has a solid track record in industrials value creation with a 3x MOIC on its last investment exiting at 9x TTM EBITDA.

- I think of it as investing in a PE fund at 50% of NAV with no leakage from fees

6. What is the EVIDENCE?

- Energy pivot evidenced by doing an appraisal in late 2024, moving the land rigs to being held for sale in 1Q, and most importantly the June 16th sale of the frac equipment

- The Transmission and Distribution investment resulted in a 3.1x MOIC in the last 8 years

- And the company has incubated other industrial businesses in rentals, engineering and fiber

7. What are the CATALYSTS for the street to realize the view?

- Collecting the line of sight cash from the frac asset sale, executing the land rig sale, potentially selling other assets, collecting the LOC cash from the PREPA settlement, and the escrow cash from the T&D sale

- Deploying the cash effectively in the future

- Investors realizing this is an undervalued industrial name with a good history of incubating industrial companies in the past

- The company did not press release the frac equipment sale, which is something that I view as a milestone for a shift in strategy

8. What is it WORTH if the bet is right?

- 2x to NAV of $6/share, more if as capital is deployed accretively

9. What is the OTHER SIDE of the bet?

- Management deploys the capital in a poor way and destroys value

10. Is MANAGEMENT aligned with Ownership?

- Wexford owns 46% and has supported the company in the past with loans and has waived its $500,000 management fee recently

- The new Chief Business Officer, Paul Jacobi, is also from Wexford

My Professional Investment Journey

My professional investment journey started at FBR after my Masters of Finance at Tulane — an alum scooped me up.

My primary mentor was my senior analyst, Rob MacKenzie, who is now the CFO of a company we use to cover. He would ask me what I learned after each conference call. I would spend hours watching him model and contemplate every assumption — he was a top ranked analyst earnings estimator and took pride in being the best. And he would allow me to barge in on almost all of his calls, with an AIM IM to ask permission of course.

The research department, led by David Khani, CFA, David Hilal, CFA & Alex Rygiel, started an Associate Program where the associates would run a monthly competition and the winners (out of 50+) would pitch to the sales force at the intraday meeting. This is where it all started. And how fortunate I was to be at a firm that believed in career training. Each small group of 5-6 (one from each sector) would pick one stock to pitch to the associate program then we'd vote on the few winners. Importantly, the senior analysts were ok with the time this took away from their main responsibilities, so long as the pitch was consistent with the rating. I was pitching a lot — and I loved it.

The pitch format (or checklist) was simple:

1) Edge/Catalyst during the month — Why are you up here? (after all SAC was the largest client and got the first call)

2) Evidence/Reasoning Bullet No. 1

3) Evidence/Reasoning Bullet No. 2

4) Evidence/Reasoning Bullet No. 3

5) Overall Thesis (1 year typically)

6) Valuation — What is the 1 year target valuation based on (sell-side style)

When I became a Senior Analyst at 26, Alex Rygiel — the co-head of the Associate Program (and the inspiration for this post) was assigned as my mentor — in addition to my VP, senior analyst who was my daily supervisor and of course my group head, Rehan Rashid. Before, I could start as a senior analyst, I/we had to hire and train two replacements. The same concept applied at Citadel, if you want to move-up, and it was encouraged, you had to back fill your seat.

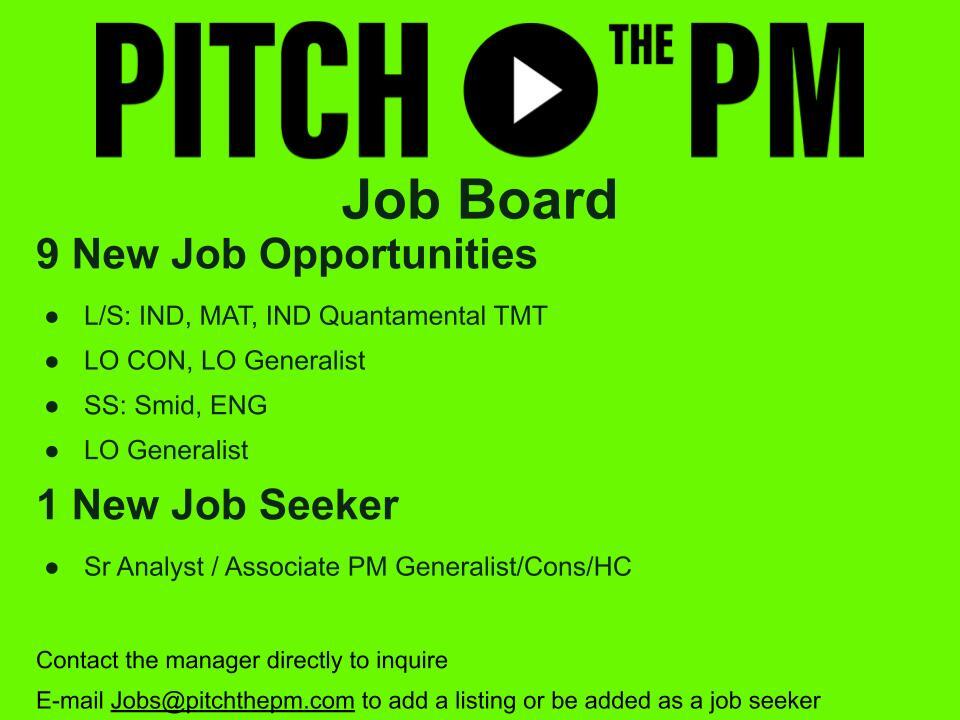

Updates to the Job Board

We are back with updates to the Pitch The PM Job Board!

Highlighting:

- Seasoned PM is launching a new team at Multi-Strat, looking to hire a Materials and Industrial Analyst. DM me for info

- Francisco Ibanez is looking to hire an Industrial Quantamental Analyst at Engineers Gate

- Jonathan Vicari, CFA is looking for an LO Analyst at Penn Capital

Great people to work for — Happy Hunting!

📌 9 New Job Opportunities:

- LO Analyst (Generalist) — Penn Capital

- LO: Associate (Consumer) — T. Rowe Price

- L/S: Analyst (Industrials) — Multi-Strat

- L/S: Analyst (Materials) — Multi-Strat

- L/S: Analyst (TMT) — Absoluto Partners

- L/S: Quantamental Analyst (Generalist / Quantamental) — Engineers Gate

- SS: Research Associate (Small/Mid Cap Generalist) — B. Riley Securities

- SS: Research Associate (Energy, E&P) — RBC Capital Markets

- Summer Intern — Mangusta Capital

🔍 1 New Job Seeker:

- 8 yrs L/S (Generalist, TMT/Cons/HC), led analyst team, Duke MBA

To see the full Job Board with all outstanding opportunities and candidates, join the Pitch The PM Job Board Newsletter to get them directly in your inbox:

|

What is Alpha?

Alpha is what’s left after you’ve stripped out all the explainable variables. Here’s a quick decomposition of what actually drives stock performance.

1. Alpha is Residual

Or what is left over after what the quantitative factors can explain. Residual is the “proper” term when used in quant land. Alpha is the “sexy” marketing term

2. Four Main Factor Categories

Currency - Stock Market - Quantitative Style Factors - Industry Factors

3. Stock Market Exposure — i.e., Beta

How much of the stock’s movement can be attributed to the movement in the stock market?

Note: Fundamental Analysts are not skilled at taking market bets, so best not to have that risk or bet in the book. Plus, the strategy is to be market neutral. Some shops use auto hedging to add beta to your book, while others will allow some tilt allowance depending on where you are and what you negotiate.

4. Quantitative Style Factors

How much of the stock’s movement can be explained by moves in quantitative factors such as Value, Growth, Short-term Momentum, Long-term Momentum, Short Interest, Hedge Fund Holdings, etc?

Note: the more factors one includes here the more that can be explained and the lower the residual, or alpha. Each “risk” model includes different factors, and it is always changing. Fundamental Analysts are historically not skilled at making style bets, that is what quants do. So best to be aware of the style factor exposure. I would make sure not style factor got over 5% of idio before I took action. Sometimes there is a factor move that is past 2-3 sigma, and those risks are often due to some macro shift or rotation.

5. Industry Factors

How much of the stock’s movement can be explained by the sector or industry’s movement?

Note: There is a debate on whether fundamental analysts have industry skill, as picking industries within a sector can be a core competency. I have seen evaluations done based on residual and based on residual + industry attribution, which is called Skill P&L.

6. Currency Exposure

How much of the stock movement can be explained by the movement in the underlying stock market currency?

Note: Fundamental Analysts are not skilled at taking currency bets, so it's best not to have that risk or bet in the book.

7. Residual (aka Alpha) is what is left over after the factors

The stock movement that cannot be explained by the factors above is what is left over or the residual (aka Alpha). It represents the company-specific attribution or idiosyncratic (idio) movement of the stock.

8. You get paid on PnL

9. You get promoted on Alpha

10. The strategy is based on generating Alpha:

Ideally, the idio is high, and the PnL and Alpha are close

|

Top 10 Learnings from Steve Cohen's Interview

Few investors have thrived as long as Steve Cohen. At a recent Goldman Sachs symposium, the Point72 founder shared timeless wisdom.

Here are my top 10 takeaways (whether you're running money or building a team)

1. Love the game

Passion is non-negotiable in investing. For most of his career Cohen "hated weekends" and was eager to get back to his desk. That intensity was the bedrock of his success.

2. Evolve your edge

Develop a repeatable process and core skill, but stay market-aware. Unlike '90s peers, Point72 shifted from big swings to tighter, risk-conscious strategies as alpha became scarce. Lesson: refine your edge as markets change.

3. Optimize for alpha generation

Cohen's multi-manager model frees investment pros to focus 100% of their time on creating alpha and finding great ideas. By handling marketing and operations centrally, Point72 lets talent do what they do best.

4. The Multi-Manager Model Is a Talent Factory

Why does it win? Focus and scale. Analysts analyze. PMs manage risk. The firm handles the rest. Talent development is treated like a farm system with a high hit rate because they know their players.

5. Betting on Adaptability Is the Long-Term Edge

Markets change. Tools change. But people resist. Steve’s longevity came from flexibility not just brilliance.

6. AI Will Widen Margins, and the Gap Between Winners and Losers

Cohen sees AI as a margin expansion tool and a secular tailwind. Firms that don’t integrate it now will fall behind.

7. Building Internal AI Tools > Buying External AI Hype

Point72 is embedding AI pros with investment teams watching workflows, then automating the manual parts. Steve isn’t betting on a silver bullet. He’s building process leverage.

8. Private Credit = the Fourth Pillar of the Firm

Equities. Macro. Quant. Now private credit. Steve sees it as the next scalable strategy and is looking to build niche-y alpha in non-obvious corners of the market.

9. Lead by developing others

Cohen now focuses on mentoring PMs and guiding new hires. He believes in nurturing internal talent and helping others think about what's possible. True leadership multiplies impact through others.

10. Spot potential in the overlooked

Cohen's Mets purchase wasn't just about sports — it was a turnaround play. By applying modern approaches and capital to neglected assets, he consistently unlocks hidden potential.

|